|

Is everyone else finding it impossible to read the internet or take part in a conversation without the coronavirus coming up? Well, this post will be no exception.

As someone who thoroughly enjoys the occasional night of self-quarantine (thank you DoorDash and Netflix), the coronavirus is the excuse I've been waiting for my whole life to stay at home wrapped in a blanket for hours on end without feeling guilty. But it turns out that buyers have other plans. While everyone everywhere seems to be in panic mode—avoiding large crowds, eating out less, working from home more, washing their hands often (ok maybe it's not all bad?), and stocking up on toilet paper like it's the end of days, Bay Area buyers seem unphased and are still going to open houses in droves, determined as ever to make their next move. Maybe it's the ridiculously low interest rates, lack of inventory, rush of activity after holding off last year, ambitious 2020 goals, or all of the above, but buyers have a renewed sense of energy and are back in the market in full force. Which means the bidding wars are making a comeback, as evidenced by these extreme examples: This mid-century modern house in Montclair got 21 offers. An Adams Point penthouse with a 500 sq ft roof terrace got 26 offers. And one charming house in Fruitvale even got 42 offers. That's FORTY. TWO. OFFERS! It truly is (March) madness out there, at least for now. With the spring market approaching, virus fears spreading, interest rates falling, important elections coming, stock market rollercoaster-ing, stay tuned to see how everything plays out. TO BE CONTINUED... In hopes of protecting the economy from this whole coronavirus fiasco, the Fed just slashed interest rates this week and they are now at a record low of 3.29%!

To put it into real-life terms, a $600k loan at today's 3.3% rate vs. last year's 4.5% rate saves you close to $412 a month for the next 30 years. That's like 537 additional rolls of toilet paper each month until you're retired! (Do the math here if you want to calculate your own financial situation and how much uninterrupted bathroom time you can afford.) But here's the catch: we can’t predict how long this will last. If this whole virus outbreak craze levels off soon, rates would likely bounce back up. On the other hand, if the outbreak continues to spread, it could drive rates down even further. It’s all unpredictable at this point, so you may want to lock in a solid rate now for buying or refi, juuuuust in case they creep up again. Lmk if you need a lender!  As coronavirus outbreaks spread across the world, investors are turning to US real estate as the more seemingly stable and safe place to park their money. Roofstock, a company that sells single-family rental homes online, has seen traffic from Asia recently spike by 500%. Germany, Australia, and the UK also showed a surge in online traffic. Chinese investors noted that our healthcare system was one of the reasons they rated US housing so highly (if only they knew..), which could prove even more valuable in the post-pandemic environment. Crossing fingers we see the other side of this soon!

In 2017, Business Insider writer Sam Dogen (also renowned author of my favorite finance and real estate blog Financial Samurai) became a stay-at-home dad after he sold his SF rental property for $2.75 million, leaving him with a $1.8 million profit after paying off the mortgage, taxes, and fees. Umm, can we say GOALS? Now a couple years later, he wants to buy property in SF again. Why now, you ask? (Or maybe you didn’t ask and I’m gonna tell you anyway?)

Well, Dogen says property prices in the US have softened and mortgage rates have collapsed. All while rent prices continue to rise! Plus he thinks the fact that 2020 is an election year, the stock market is thriving AF, and the amount of foreign buyers has dramatically decreased, all point to now being a good time to start looking into purchasing. He listed about 87** other reasons if you’re interested in reading all of them (**ok fine slight exaggeration, but honestly, there were a lot and they were all pretty convincing). *Disclaimer: Every economist, journalist, and psychic will have varying degrees of optimism and pessimism about where the housing market is going—up, down, all around. If you want to compare different points of view and form your own educated prediction, here are a few other market forecasts to satisfy your inner nerd: Realtor.com, Redfin, Forbes, Freddie Mac, and Zillow.  Inquiring minds want to know. To answer our burning questions, Estately mapped out the relative cost of living near BART, compiling the average sale price per square foot for all the houses, townhouses and condos that have sold within a one-mile radius of each BART station over the past six months.

(If squinting at the blurry numbers on the map is hurting your eyes too, click here for a larger view.) Here are the ten “most expensive stops” and relative commute times to Downtown San Francisco (defined as Embarcadero station): 1. Embarcadero – $1,191 per square foot (0 minutes) 2. Montgomery Street – $1,149 (2 min) 3. Powell Street – $1,099 (4 min) 4. 24th Street/Mission – $1,001 (9 min) 5. 16th Street/Mission – $998 (7 min) 6. Civic Center – $994 (6 min) 7. Millbrae – $854 (25 min) 8. Glen Park – $817 (11 min) 9. SFO – $735 (32 min) 10. Rockridge $704 (20 min) And the ten least expensive: 1. Pittsburg/Bay Point – $219 per square foot (62 minutes from Downtown San Francisco) 2. Richmond – $258 (35 min) 3. Coliseum – $270 (20 min) 4. North Concord/Martinez – $306 (56 min) 5. Concord – $317 (43 min) 6. Hayward – $347 (32 min) 7. South Hayward – $356 (36 min) 8. San Leandro – $366 (24 min) 9. Bay Fair – $376 (28 min) 10. Castro Valley – $406 (32 min) BART is also extending from Fremont into Silicon Valley, where new housing, commercial and retail developments are already being planned around the future South Bay BART stations. Home values nearby will probably increase, along with the number of commuters crammed into a sardine can of a BART train.  (Twin Peaks, that is.)

Good news for buyers: the hottest housing market in the country might finally be cooling off. According to Redfin, home prices in San Francisco declined last month for the first time in four years. The median home price in the area dropped 1.8% in March from last year to $1.04 million. Quite a big difference from last year when prices in the market averaged 15% growth. Sales also took a hit, sinking 22% in March -- which normally marks the start of the busy home-buying season. While it's still a seller's market in San Francisco, homes are sitting on the market longer and inventory of unsold homes is at its highest in four years. Economists and housing experts credit the shifting real estate climate to Wall Street's recent volatility, overvalued tech companies, and slowing interest from overseas buyers.  Oh, that's it? Apologies in advance for the buzzkill, but according to a new Charles Schwab survey, to be considered "wealthy" in the Bay Area, you need a net worth of at least $6 million. A net worth of $1 million is the baseline for being "comfortable." That's all, no big deal.

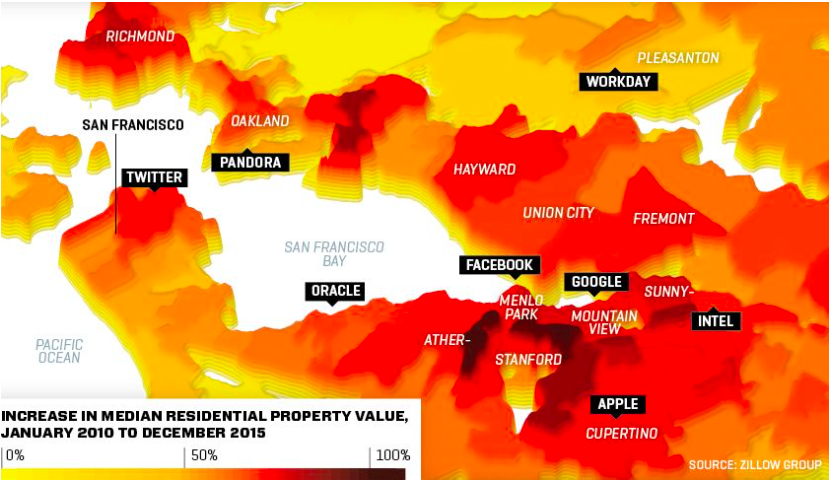

Charles Schwab surveyed 1,000 Bay Area residents aged 21 to 75 in Alameda, Contra Costa, Marin, SF, San Mateo, Santa Clara and Solano counties. The survey asked what residents considered enough money to be "wealthy" vs. "comfortable." They believed $2.5 million was the average needed to be wealthy in other parts of the country. The survey unsurprisingly found that locals are shocked by the cost of living here. 86% said the cost of living is "unreasonable" and 55% said living in the Bay Area makes it "difficult to reach their financial goals." To counteract these depressing stats, the majority also believe this is a prime place for career growth and innovation, and the Bay Area's economy is better than the national one.  While SF is notoriously known for its rapidly rising home prices, the city's neighboring towns have far exceeded its growth. Between January 2010 to December 2015, home prices rose more than 70% in some SF neighborhoods, according to Zillow. But in Palo Alto between Stanford and Google, prices climbed 104% - and 101% in CEO tech haven. Let's see what the rest of 2016 brings.

Janet, as in Janet Yellen of the Federal Reserve (see confused lady pictured above for reference). Stockholders, homebuyers, and finance nerds everywhere are biting their nails and on the edge of their seat as they brace for the Fed's next policy meeting on March 15-16th. This is when the Fed will decide whether to hike short-term interest rates again after raising rates in December off zero for the first time since the 2008 financial crisis.

Many were hoping for an oil production cut to serve as a catalyst for higher stock prices, but that idea has been nixed for the time being. The confidence that rate hikes will be put on hold also helped the stock market rebound since the recent mid-Feb low. To keep the country in suspense, the Fed said on Tuesday night that they "simply do not know" if they will hike rates or not. Investors want the economic data (on GDP, personal income and spending) to show evidence of a perfect middle ground - that a recession isn't looming, and at the same time, that the economy isn't heating too much either. Until then, the market continues to be at the mercy of oil prices and Janet. Especially in the Bay Area. But you already knew that. Redfin found that since 2001, the average amount of time homeowners stayed in their current residence more than doubled from 4 to 10 years, creating less opportunity for first-time home buyers. Low rates and improving economic conditions boosted demand in 2015, but also caused homeowners to refinance under historically favorable terms and to invest in improvements rather than move.

Here are some Bay Area highlights of Redfin's findings:

|

MICHAELA TO

510.266.2802

mto@MichaelaTo.com

1900 Mountain Blvd. Oakland, CA 94611

DRE# 01883913

510.266.2802

mto@MichaelaTo.com

1900 Mountain Blvd. Oakland, CA 94611

DRE# 01883913

Copyright 2014-2024. All rights reserved.