Janet, as in Janet Yellen of the Federal Reserve (see confused lady pictured above for reference). Stockholders, homebuyers, and finance nerds everywhere are biting their nails and on the edge of their seat as they brace for the Fed's next policy meeting on March 15-16th. This is when the Fed will decide whether to hike short-term interest rates again after raising rates in December off zero for the first time since the 2008 financial crisis.

Many were hoping for an oil production cut to serve as a catalyst for higher stock prices, but that idea has been nixed for the time being. The confidence that rate hikes will be put on hold also helped the stock market rebound since the recent mid-Feb low. To keep the country in suspense, the Fed said on Tuesday night that they "simply do not know" if they will hike rates or not. Investors want the economic data (on GDP, personal income and spending) to show evidence of a perfect middle ground - that a recession isn't looming, and at the same time, that the economy isn't heating too much either. Until then, the market continues to be at the mercy of oil prices and Janet. Especially in the Bay Area. But you already knew that. Redfin found that since 2001, the average amount of time homeowners stayed in their current residence more than doubled from 4 to 10 years, creating less opportunity for first-time home buyers. Low rates and improving economic conditions boosted demand in 2015, but also caused homeowners to refinance under historically favorable terms and to invest in improvements rather than move.

Here are some Bay Area highlights of Redfin's findings:

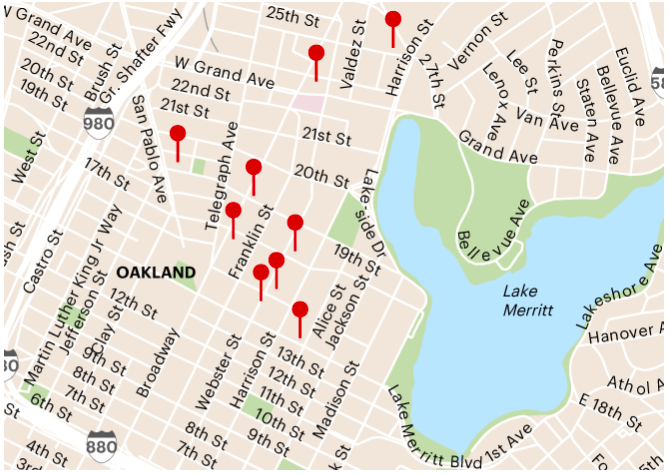

To help remedy the housing shortage, a rush of proposals for new Oakland towers have been submitted. It will potentially add over 3,000 residential units to downtown, becoming one of the largest building booms in the city's history. The projects would transform lowrise buildings and parking lots into a fancy glass, steel and concrete skyline. When asked about her hopes and dreams for Oakland, Mayor Libby Schaaf said, "I like tall buildings, especially near transit." In other words, she supports denser housing downtown and hopes to see 17,000 units of new housing built in Oakland within the next 8 years. See map below for the downtown highrise pipeline:   Stephen Curry, the superstare behind the record-breaking Warriors team, recently bought a modest $3.2 million home in Walnut Creek. The house came on the market in April for $3.988 million and was more recently priced at $3.65 million. It previously sold for $2.5 million last year. With 5 bedrooms, 5 bathrooms, and 8,000 square feet sitting on an acre of land, this two-story Mediterranean estate includes a 2,300 bottle wine cellar for lots of wine guzzling and 4 fireplaces for some more s'more making. Just in time for the holidays.  Bay Area market is slowing down as homes are seeing fewer offers. According to Redfin, many Bay Area residents pay for houses with stock, so that willingness to bid $300k over asking price is being limited by the volatility of the stock market.

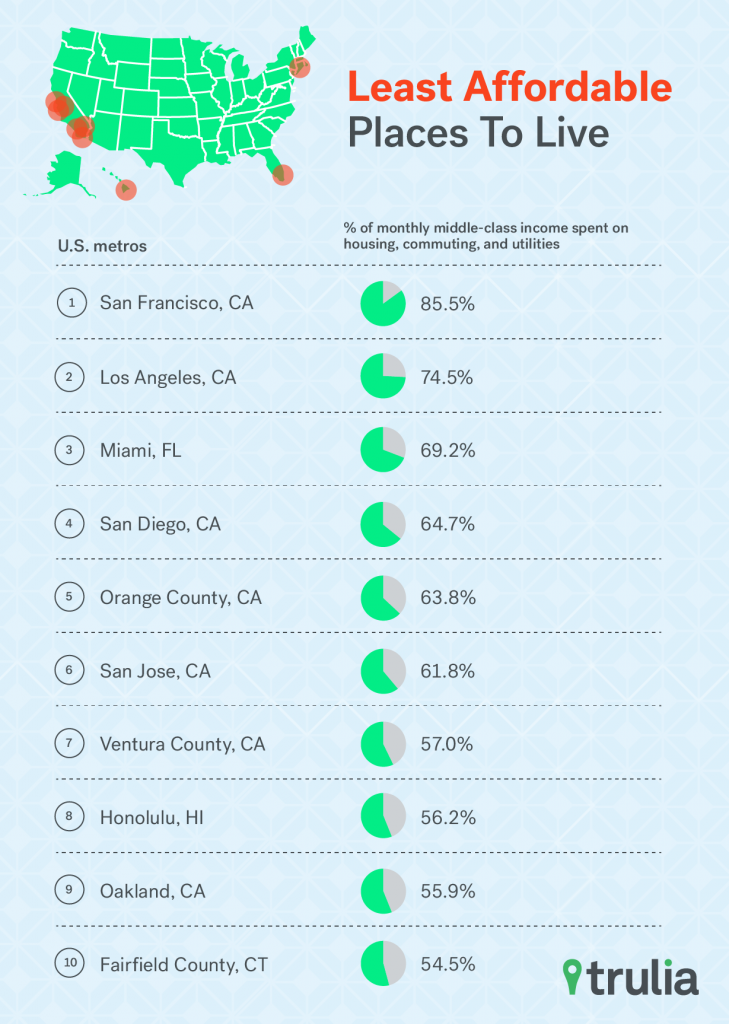

"The spring frenzy has been so frenzied for the last three years that there is a certain exhaustion that enters into buyer mentality. They're tired of not winning. There's fatigue on buyers' part and it lessens the competitive environment," Glen Kelman, the CEO of Redfin said. Instead of the bidding wars of 15-20 offers on each property we were seeing only a few months ago, homes are getting 3-5 offers instead. While still undoubtedly a competitive market, the buyers' odds just got a whole lot better. Kelman also added, "The market has gotten frothy so there will be a period of softening. We always say San Francisco defies the laws of physics. In other markets, what goes up must come down. Here, it just flattens out." The same goes for Oakland where there is still so much job creation and high housing demand that we will most likely not see home values drastically decline anytime soon. Tired of seeing the Bay Area on lists of "Least Affordable Places to Live" yet? Welp. That's too bad, because here's another one. (Spoiler alert: SF, San Jose, and Oakland made it to the top 10.) New data from Trulia finds that the average-earning SF resident has to pay 77% of their monthly salary toward the average mortgage as of August 2015 (assuming 30-year loan, 4% interest rate, property taxes, and insurance). That's an insane 20% increase from just a year ago. Trulia factored in the costs of utilities and of commuting, which SF (and San Jose) has among the lowest costs for, so some of what homebuyers lose in affordability are made up by cheaper commuting and utility costs. Still, added all together, average mortgage, utilities, and commuting add up to 85.5% of the median income earner's wages. That leaves only 14.5% left over for everything that isn't housing yourself, getting to and from the office, and keeping the heat and lights on. In comparison to Oakland, where these expenses make up (only) 55.9% of a resident's income, it almost seems as if Oakland is an inexpensive place to live. But don't worry, Uber will be sure to change that soon.  Finally some good news for the discouraged and disgruntled Bay Area buyers! Zillow's latest numbers show that the nation's housing market is actually starting to level off. While the Bay Area is still one of the hottest markets in the nation, we're seeing a decline in home appreciation growth and the market returning to normal.

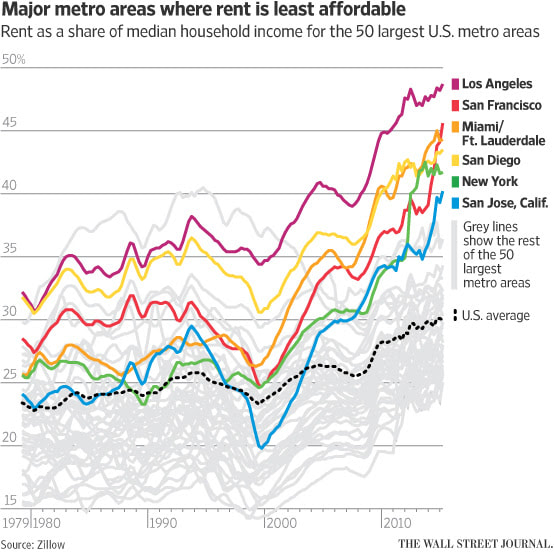

Falling home valuations and increased home inventory are expected to spur renters to buy, especially given the dramatic increases in rents. SF area rents jumped over 14% to $3,285, proving to be painful - both financially and physically - as tenants go as far as to skip their dentist and doctor visits just to pay their landlords. Because what good is a healthy body if there is no roof to shelter it? The first world problems of the middle class are real! And of course I cannot end this post without a shameless plug: Take advantage of the slowing market and find your next home here! The rent-to-income ratio is the highest EVER (or at least since 1979, because Zillow only has data from that far back). Renters on a national average can expect to pay 30.2% of their income on rent, while renters in the San Francisco metro area pay a whopping 47% of their incomes on rent (only trailing behind LA). Thanks to the perfect combination of increased demand and limited supply as income levels stay relatively flat, the outrageous proportion of incomes spent on rent will continue to rise as rent increases too. These unaffordable rents are making it hard for people to save for a downpayment, retirement, and even basic expenses like food and healthcare.  The longer you wait to buy a home, the more it can cost you. A recent report published by Realtor.com indicates that the financial consequences of postponing or passing on a home purchase in the current market could be quite costly. It suggests that, on average nationally, the penalty of waiting to buy for one year is almost $19,000 and nearly $54,000 for a three-year delay. Meanwhile, the estimated wealth that a person would garner over 30 years of homeownership is over $217,000.

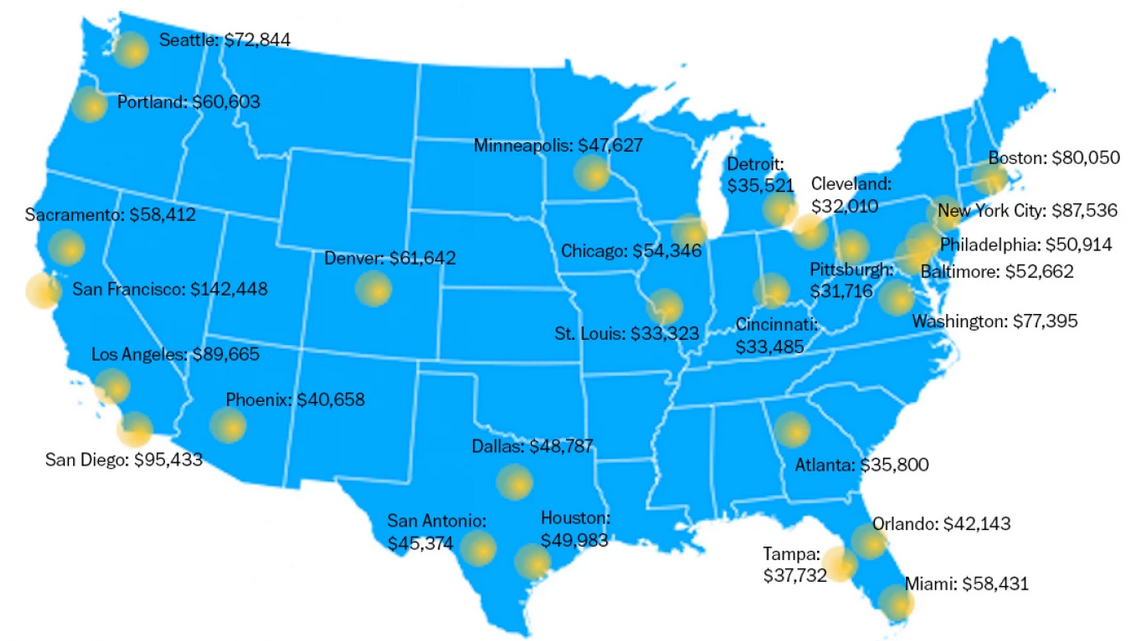

Current market conditions give buyers the opportunity to build substantial wealth in the long-term, compared with renters and later buyers. Affordability is at its peak now as both interest rates and price appreciation are on the inevitable rise, and buying a home enables a buyer to avoid high and escalating rents. So, don't be a snoozer/loser! But as a disclaimer: don't be irrational either. Hold off on the purchase if you don't expect to remain in the home long enough to cover the transaction costs of buying, selling, and market fluctuations. With all that said, find your next house here! And the award for The Most Unaffordable Place To Live goes to...the Bay Area. You are shocked, I can tell. To buy a median-priced home of $742,900 in the Bay Area (which includes SF, San Mateo, Alameda and Contra Costa counties), all you need to make is a measly income of $142,448 a year. That's it! On the opposite end of the spectrum, Cleveland is the most affordable metro area on the list, where you can buy a huge roof over your head with just a slightly lower salary of $32,010. But then....you'd have to be a Cavs fan. And who wants that? (See appropriately colored map below for the salary needed to live in other major metros around the country.)  |

MICHAELA TO

510.266.2802

mto@MichaelaTo.com

1900 Mountain Blvd. Oakland, CA 94611

DRE# 01883913

510.266.2802

mto@MichaelaTo.com

1900 Mountain Blvd. Oakland, CA 94611

DRE# 01883913

Copyright 2014-2024. All rights reserved.